Deutsche Bank's toxic derivatives

30 November 2007

Readers may recall our article of 8-Jun-05, CSFB's Toxic Convertibles, in which we detailed a series of value-destroying toxic convertibles in which the companies issued bonds with a floating conversion price to the investment bank. CSFB (now Credit Suisse) made a textbook public relations response, huffing and puffing and "seeking legal advice" over our article, which also put the media at risk if they reported what we said. But the bank never sued. Our article was right, and what we said was fair comment.

The passage of time shows that our article had the desired effect - Credit Suisse has not done another of these deals in HK, and we have not seen a single convertible bond issued by a HK-listed company with a floating conversion price since then. A few have "reset" clauses, allowing the conversion price to be reset downwards at one or more fixed times (typically on the anniversary of issue), but none is floating. Some of the issuers featured in our article, including EganaGoldpfeil (0048) and Tack Fat (0928) have since been found to have other problems.

We subsequently found vindication in a report by the Securities and Futures Commission on the 2005 work of the Stock Exchange Listing Division. In the report, dated Dec-06 but not published until 4-Apr-07, the SFC said (para. 48, p.12):

"In the last few years, several companies issued a particular type of convertible note, now commonly referred to as "toxic convertibles"... In the absence of other factors, each conversion is likely to lead to a reduction of the issuer's share price and an increase in the number of shares into which the remaining notes can be converted, resulting (because of the falling share price) in a spiral of further dilution of existing shareholders and reduction in share prices. In the worst-case scenario, the notes are converted into shares at the par value and the convertible noteholders may end up holding almost all the company's shares."

Credit Suisse has cleaned up its act, but unfortunately that episode has not deterred at least one of its competitors from hawking exotic products to small and unsophisticated companies, despite the reputational risk such behaviour carries, as we will show in this story. These are not the products that you see many large companies buying, for the simply reason that they know better.

Deustche Bank (DB) has sold products to at least three (there may be others) small listed companies, all industrial stocks from Fujian, and all of which have surplus cash on their balance sheets. Whether they have also sold such products to private bank clients we do not know. These products are highly complex with no liquid market and no easy way for the client to price them. The products are similar in each case, so we will start with the company we know best. Later in this article, we'll cover some more companies which have bought complex derivatives from unnamed banks.

Sinotronics

Sinotronics Holdings Ltd (Sinotronics, 1195) is a maker of printed circuit boards based in Fujian. At 30-Dec-06, it had net cash of RMB382m. In note 5(a) of its financial statements for the year ended 30-Jun-07, Sinotronics disclosed that the "finance costs" in its income statement included fair value losses on derivative financial instruments of RMB38.959m. This knocked about 22% off its pre-tax profit for the year.

Note 24 discloses that there were two products involved. The first, in Feb-07, is a 5-year swap with a notional amount of HK$390m (US$50m). Sinotronics gets an up-front payment of 10% of that, or HK$39m. Sinotronics pays 9% p.a. on the notional amount for the 5-year term (on a semi-annual basis), and the bank pays an introductory or "teaser" rate of 7% p.a. for the first 6 months. After that, for the next 4.5 years, the bank pays 7% p.a. multiplied by a fraction between 1 and zero, representing the proportion of the days in each half-year period in which the 10-year HKD Swap Rate is greater than the 2-year HKD Swap Rate.

We pause to explain for non-professional readers, the "Swap Rate" is the fixed interest rate which can be achieved in return for an obligation to pay the prevailing floating interest rate throughout the period of the swap. It is usually very close to the yield on a top-rated bond for the same period.

So what this product was betting on is that the "yield curve" (a graph plotting the yield against the maturity of bonds) curves upwards. When the 2-year rate is greater than the 10-year rate, then the curve is pointing downwards, and this is known as an inverted yield curve, which happens from time to time, often preceding economic recessions.

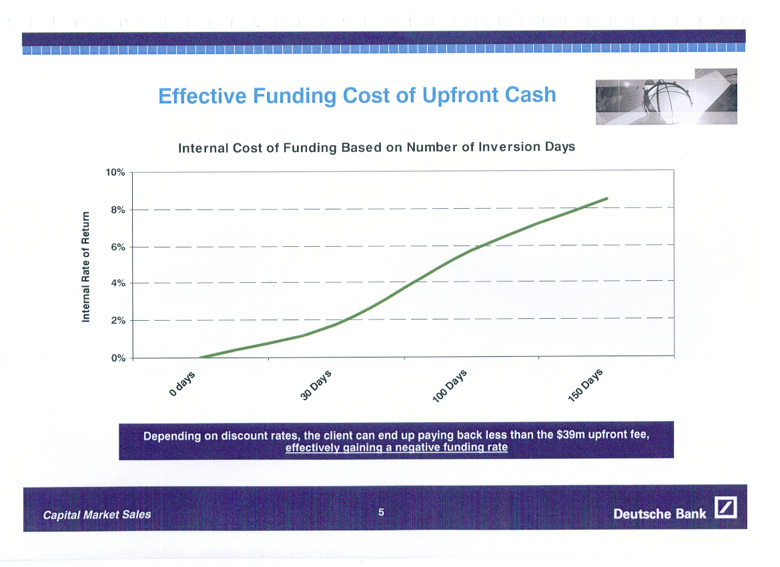

In its English presentation to Sinotronics, a company run by mainlanders, DB presented a rather attractive graph of the "Effective Funding Cost of Upfront Cash". It sounds just a like a loan, doesn't it? The graph plotted "internal cost of funding" versus "Number of Inversion Days". Here's the graph, so you can judge for yourself:

Notice how that curve seems to take a gentle "S" shape and taper off as time goes on, reaching 8% with 150 days inversion? That might seem like quite a good deal to someone with little understanding. After all, 150 days is nearly a half-year period, so presumably that's about as bad as it can get, and paying 8% isn't too bad if you can get a better return on the funds. You might even get lucky and only have a funding cost of 0%.

But wait. That graph is, in our view, highly deceptive. First of all, notice that the x-axis is not linear - the chart shows equal spacing between 0, 30, 100 and 150 days. That's why you see a kink in the curve. Second, and most importantly, the only way we could reproduce that graph is by realising that 150 days is not part of a half-year, but part of the entire 5-year period, based on calendar days. So what you are seeing is only a tiny part of a graph which should extend out for the maximum 1825 days (ignoring leap days).

We ran the calculations on a spreadsheet, attempting to replicate this graph, and produced a very similar graph for the first 150 days, using the same non-linear spacing on the x-axis:

That's close enough. But now look what happens if you use a linear scale, and show the full possible range of outcomes in the 5-year period:

This shows the toxic downside of the DB derivative. In the worst case, if the yield curve is inverted throughout the 5-year period, then in return for the $39m upfront payment, after paying a net $3.9m for the first half-year, the client pays $35.1m per year (9% of the notional amount), resulting in a loss of $122.85m, with an internal rate of return for the bank (and cost to its client) of about 79% per year. Even if the curve is only inverted for 20% of the time (365 days), the funding cost rises to 20% per year, far more than the firm would have to pay for bank borrowings.

The area in the DB graph is just that bit in the blue box (looks rather like their logo, doesn't it?) - the rest was not shown to the client. Incidentally, throughout the presentation, DB refers to "client" but in the disclaimer on the back page (if the client can read English) the client becomes just a "counterparty" and there we find the attempted get-out words "in making this evaluation you are not relying on any recommendation or statement by us". The contract we have seen has similar disclaimers. However, a court might take the view that if a client was incapable of reading English, and had signed an English contract based on an English presentation book and a verbal presentation from a bank, then he was entitled to rely on the verbal explanations he was given by the bank's salespersons, and if those contradicted the contract then it might be voidable.

Now of course, we all hope that markets will remain normal, and the yield curve will not be inverted for long, but the downside risk in terms of funding cost makes this nothing more than a highly leveraged gamble. There is almost no upside (the best case is a funding IRR of 0%) and horrendous downside.

The second product

As if one sale wasn't enough, DB in April sold Sinotronics a second product, with a notional amount of US$100m and an up-front payment to the client of US$10m. In this 5-year deal, the bank pays 8% p.a. of the notional amount semi-annually, while the client pays 10% for the first half-year, and then it gets complex. In each half-year period, you take the year-on-year change in the "Deutsche Bank Pan-Asian Forward Rate Bias Index" (which as you guessed, is produced by DB). You then subtract 1% from that return, and multiply it by 5, and then subtract that from 10%. The result is capped at 13% with a floor of 0%.

Is that clear? As Alan Greenspan once said, "If I have made myself clear, then I have misspoken". DB describes the product in its pitch as "this simple swap".

For non-professionals, a forward rate agreement, or FRA, is an agreement between two parties to settle the difference between an agreed (fixed) level of interest and an actual future level of interest, determined from the market on a future effective date. For example, Anna might expect that in six months' time, the one-year LIBOR (London Interbank Offered Rate) will be 4%, so she agrees with Bob that in six months time she will pay him (or he will pay her) the difference between 4% and the actual one-year LIBOR on that date. Since the interest difference is known at the start of the lending period (the effective date of the contract), the payment is made on the effective date, discounted for the interest it would earn up to the end of the period. Except, of course, that Anna and Bob are ordinary people who wouldn't have a clue what an FRA is.

Now according to the presentation, money markets are not efficient, and "forward rates have a large tendency to over-predict the future realised interest rates". In other words, the actual future rates turn out to be not as high as the prices in the FRA market predict. There are several academic papers out there suggesting this, but most of them are focused on forward foreign exchange rates rather than interest rates themselves. Regardless of the details of this supposedly golden opportunity, whenever a bank tells you they have discovered a systemic (rather than brief) mis-pricing of markets, and have packaged it up in order to provide access to clients, your response should be:

- So why don't you exploit it yourself? Are you short of money?

- If the anomaly is well-known, then how come it has not already been removed by arbitrageurs such as hedge funds and banks?

So on the basis of the Forward Rate Bias theory, DB created a series of indices, one of which is the Pan Asian index, covering the equally weighted average of Thailand, South Korea, Taiwan, Malaysia, Singapore and Hong Kong. In each market, the index is based on receiving the 12-month forward 12-month Interest Rate Swap contract, holding it for 3 months, and then unwinding it as a 9-month forward contract and starting again. Any gain resulting from the difference between those rates is added to the index. We don't know how liquid such markets are or where they get the quotes from, but lets assume they are legitimate.

If however, this anomaly is removed (that is, markets are efficient after all), then the index becomes a flat line with zero long-run return, in which case the formula in this toxic product becomes 10-5*(0-1)=15%, so the cap of 13% applies. From that you deduct the 8% paid by the bank to the client, leaving a net rate of 5%. That's on the notional amount of the product, so in return for an up-front payment of US$10m, the client has to pay US$1m after six months, and then US$5m p.a. for 4.5 years, for a total net loss of US$13.5m (HK$105m).

That's an internal rate of return for the bank (and cost to the client) of 39.0% per year. This is something that DB described as the "worst case scenario" in its presentation, but it is in fact a scenario which would be expected if markets are efficient. They would have to be inefficient to the tune of more than 0.4% per year before the funding cost starts to decline from 39% p.a.. Incidentally, DB calculated the worst-case IRR at 35.82%, but that implies they used a semi-annual rate. IRRs are conventionally quoted on an annual percentage rate (APR) basis. DB didn't include a graph of IRR in its presentation, so we are producing one to show you:

As the graph shows, it is only if the index gains 0.9% annually that the IRR comes down to a reasonable funding cost of about 7.7% p.a. To get the IRR down to zero, the index would need to return 1% per year, indicating a substantial mis-pricing of the FRA market. Beyond that, there is the theoretical potential for the client to make a profit of up to US$35m if the markets are inefficient to the extent of 3% per year, but reality is highly unlikely to produce that. DB claimed that its index has returned 1.18% p.a. since inception in Aug-99. However, most of that was in the earlier years up to Mid-2003, when central banks were aggressively cutting interest rates after the tech bubble burst. It is not surprising that during that period, the FRA market over-predicted rates, as the central banks cut rates more sharply than the market expected.

Stupidity discount

This is the second time that Sinotronics has bought a toxic deal - it was one of the issuers of toxic convertibles to CSFB. That deal was eventually ended in Jul-06 when, by agreement, Credit Suisse agreed not to require an additional tranche of bonds to be issued, and converted the first tranche at $0.909 per share, expanding the share base by 85.544m shares, or 18.3%, and sold them for $1.02 each (close to market price) to the controlling shareholder, Lin Wan Qaing (Mr Lin). Mr Lin has since sold 140m shares, cutting his stake from 66.6% to 41.0%, a large portion of which was purchased by Atlantis Investment Management, which now holds over 15%. Webb-site.com editor David Webb currently holds over 5% of Sinotronics.

Since Sinotronics first revealed the derivatives in the results announced on 24-Oct-07, the shares have fallen 39% from $1.77 to $1.08, wiping HK$385m off its market value. That's despite the fact that operating profit rose 18% year-on-year, with turnover up 32%. Beneath the appallingly inept financial management, there is a growing business on an expansion path, which is why your editor held the stock in the first place. After the toxic convertibles, we thought they had learned a lesson not to do things they don't understand, but apparently not. A stupidity discount is now appropriate, and the market price reflects that. They would need a change of management to overcome it.

Getting out of it

The biggest problem with such exotic products is that there is no ready market for them, so the client has absolutely no idea of what a product is really worth, except by observing the collapse in their share price after they disclose that they bought it. Nor do they know how large the bank's profit margin is. How does the client know that the upfront payment in the product is a big enough compensation for the risk they are taking? They don't, and once the client has signed a binding contract, it is locked in (unless they can get a court to void it). In its disclaimer, DB says "While we may quote an unwind or bid price for this transaction (which we have no obligation to do), prices quoted may materially differ from our economic assessment of this transaction or its component parts". In other words, we know what it's worth, but that isn't what we'll pay you.

In order to produce interim and annual reports, the client has to go back to the bank and ask for a valuation of the product - in essence, the price at which the bank would be willing to buy it back. In each case we identified, this resulted in an immediate and substantial loss of fair value.

According to management, on 2-Nov-07, Sinotronics asked DB for a quote for unwinding the two products. The indicative verbal quote, together with previous payments, would have resulted in an overall loss of about HK$71m (including the amount already booked in the 30-Jun report) compared with the upfront payments received of HK$117m. You could probably do better borrowing money from a Macanese loan shark.

Now let's move on to the other two cases involving DB which have so far come to light...

Spread Prospects

Spread Prospects Holdings Ltd (Spread Prospects, 0572) is, quite literally, a tin-pot little company. It makes tinplate cans for the packaging of foods and beverage and is based in Fujian. At 31-Dec-06 (according to the accounts), they had net cash of RMB312m. On page 18 of its interim report for the six months to 30-Jun-07, it disclosed that it had entered into exactly the same pair of products, as Sinotronics, with maturity of 28-Feb-12 for the non-inversion bet, and 23-Apr-12 for the Forward Rate Bias bet, although the latter was smaller, with a notional amount of US$50m rather than $100m in Sinotronics case. The timing is remarkable - just 14 and 4 days respectively after the Sinotronics contracts. During the period, Spread Prospects received up-front payments totaling HK$78m and booked a loss of RMB15.469m on the products. They certainly didn't need the cash.

Incidentally, the IPO of Spread Prospects in Jun-03 was sponsored by Upbest Securities Co Ltd, which is owned by Upbest Group Ltd, which featured heavily in our recent article on Egana.

We can make a past connection between Sinotronics and Spread Prospects. According to the prospectus of Spread Prospects dated 10-Jun-03, Mr Tong Yiu On owned 21m shares, or 5.48% of the post-IPO share capital, which was acquired on 8-Jul-02 for US$339,500 (HK$2.65m), which works out to a P/E of just 1.18 times the previous year's earnings. A year later, at the IPO price of HK$1.23, the shares were worth HK$25.83m. Mr Tong is the Finance Director of Sinotronics. He sold 15m Spread Prospects shares at $0.81 per share on 5-Feb-04 shortly after the lock-up expired, dropping below the disclosure threshold.

Spread Prospects is currently 5% held by Concordia Advisors (Bermuda) Ltd and 8% by the SFP Asia Fund run by Symphony Financial Partners.

First Natural Foods

First Natural Foods Holdings Ltd (FNF, 1076) is a Fujian-based food processor. Page 19 of the interim report for the six months dated 30-Jun-07 states:

"The Group had a structured financial instrument with the notional principal amount of US$100,000,000 (approximately RMB753,000,000). Its tenor has 5 years. Coupon payment is semi-annually. The first coupon rate is fixed at 2% and thereafter the subsequent coupon rate are floating based on Deutsche Bank Pan-Asian Forward Rate Bias Index (AFRB Index). Nonetheless, the Group has capped at 5% and floored at 0% for floating rate coupon payments. As at 30 June 2007, the fair value of the structured financial instrument was RMB94,394,000."

That instrument was booked as a liability, and FNF booked a fair value loss of RMB19.166m in the report - in other words, a liability of RMB75.228m had grown to RMB94.394m since the product was issued some time in that six-month period.

We can make a connection between Sinotronics and FNF. According to page 57 of its IPO prospectus dated 30-Jan-02, on 11-Jul-01, Mr Lin, Sinotronics' then Chairman, and Mr Tung Fai (Mr Tung) jointly (in the ratio of 60:40) acquired an effective 35% pre-IPO stake in FNF for just US$1.75m (HK$13.65m). Mr Lin held 21% and Mr Tung 14%, which were diluted in the IPO to 15.75% and 10.50% respectively. The IPO was priced at HK$0.73 per share, valuing FNF at HK$800m, so Mr Lin's stake was worth HK$126m, compared with the $8.19m he paid for it just 7 months earlier! On top of that, the pre-IPO company paid a dividend of RMB75.61m (then HK$71.33m) to its shareholders in Sep-01, so Mr Lin would have been due HK$15.0m of that - or twice what he paid for the shares two months beforehand. Don't ask why the vendor sold for such a low price.

Mr Lin was a non-executive director of FNF from 10-Oct-01 to 3-Jun-02. He is no longer a disclosed shareholder of FNF.

Mr Tung seems to be a serial IPO man. He joined China Agrotech Holdings Ltd (China Agrotech, 1073) in 1998, before its IPO, and was an executive director until 31-Dec-02. Overlapping with this, in Jun-00, he joined Techwayson Holdings Ltd, now known as The Quaypoint Corporation Ltd (2330), ahead of its IPO. That company was listed on 8-Feb-01 with Mr Tung as an executive director. He left them on 4-Nov-05. Overlapping with that directorship, in Jan-03 he joined Fu Ji Food and Catering Services Holdings Ltd (1175), ahead of its listing on 17-Dec-04, and he's still there as an executive director.

Incidentally, Raymond Tong Hing Wah, the CFO of China Agrotech, has been an INED of Spread Prospects since its IPO.

FNF is currently held 7% by SPF Asia Fund (yes, them again) and 5% by Veer Palthe Voute of the Netherlands, part of Allianz Group. On 14-Sep-06, FNF issued a 5-year convertible note for HK$116m to DKR SoundShore Oasis Holding Fund Ltd. Up to 18-Sep-07 $56m had been converted.

Panva Gas

Writing about these cases brings to mind other companies which have been burnt by derivatives, including Panva Gas Holdings Ltd (now Towngas China Co Ltd, 1083). We don't know who the bank in that case was. The 2005 annual report revealed that they had made some kind of bet on the difference between the 2-year and 30-year US$ swap rates, resulting in a HK$208.1m loss on the position that year. The formulae in note 25 of the financial statements are unintelligible, but the loss was clear. In the 2006 annual report, a further write-down of $124.2m was taken when the group early-terminated the contracts on 21-22-Sep-06 by making payments totaling HK$433.6m; see note 24 of the financial statements.

Dream

Another disaster-prone company is stuffed toy maker Dream International Ltd (Dream, 1126), which should probably be renamed Nightmare International Ltd.

In 2003 Dream entered into a "long-term structured deposit contract" with an unnamed bank to place a total of US$15m in installments over 3 years to Jul-05, placing US$8m by 31-Dec-03 and topping it up to US$12m by 31-Dec-04. Interest was paid at 6% in the first year and in subsequent years at rates "based on" LIBOR. Whenever you see the words "based on" in corporate disclosures, you can fairly bet that it doesn't mean "equal to". In early 2005 they terminated the contract, paid a penalty of US$1.5m and booked a revaluation loss of HK$8m in the 2004 accounts (notes 3 and 19) and a loss of HK$3.7m in the 2005 accounts (note 18(i)).

Flushed with the success of its first foray, in 2005, it entered into another "long-term structured deposit" with a principal value of US$12m (HK$93.3m). This had a teaser rate of 6.5% for the first year and then for the next 11 years a rate based in an unspecified way on the spread between the 30-year and 10-year US dollar swap rates - a yield curve bet. This was paying only 1.3% at 31-Dec-06, and had been written down to a fair value of HK$69.2m as shown in note 11 of its annual report. As of 31-Dec-05, Dream estimated (note 29(c)) that a 0.05% change in the spread between 10-year and 30-year rates would result in a HK$4m loss. No such disclosure was made in the 2006 report.

The Bottom Line

There are two sides to this behaviour, listed companies and banks, and both are to blame. Listed companies have absolutely no mandate to invest shareholders' funds in long-term (more than 1-year) deposits, structured or otherwise, or to put shareholders' money at risk in speculative derivative instruments. If they have surplus capital beyond their budgeted requirements, then it should be returned to shareholders by way of dividends. Controlling shareholders can then take their dividends and do whatever they like with it, without affecting minority shareholders' wealth. The only time that the use of derivatives can be justified by a listed company is if it is part of an exercise to reduce risk (such as hedging of commercial transactions in foreign currencies), not to increase risk.

On the other side, banks of global standing such as Deutsche Bank should know better than to peddle such toxic instruments to ignorant customers, whether they are listed companies or private individuals. A company cannot be assumed to be a sophisticated investor just because it is listed. If it is run by unsophisticated directors then it is just the same as if the product was sold to them personally. There is a clear and well-accepted standard of "suitability" in the investment advisory industry, which requires that advisers should only sell products to clients who they reasonably believe are capable of understanding the product and all its risks, and where the product matches the needs and circumstances of the client. Morally and reputationally, you can't get out of that by pitching a product with a glossy presentation and then claiming in the small print not to be advising the client on the merits of the product and suitability for the client's needs.

Clearly from the risk profile, these products are not suitable for listed companies. They don't reduce risk, they increase it, so they fail the suitability test. Furthermore, in our view, anyone who understood the risks in the Deutsche Bank products would be out of their mind to buy them on those terms. The almost immediate loss of value (just a few months into a 5-year term) indicated by the quotations used for fair value accounting indicates how overpriced the products were in the first place.

Let this article serve as a warning to all banks and listed companies out there - if we find this behaviour again, we will name you and shame you. Meanwhile, if Deutsche Bank wishes to do the decent thing, then they should cancel the contracts without loss to the their clients.

© Webb-site.com, 2007

Organisations in this story

- DEUTSCHE BANK AKTIENGESELLSCHAFT

- DREAM INTERNATIONAL LIMITED (HK)

- Fresh Express Delivery Holdings Group Co., Limited

- Future World Holdings Limited

- Imperial Pacific International Holdings Limited

- Kingwell Group Limited

- Towngas Smart Energy Company Limited

People in this story

Sign up for our free newsletter

Recommend Webb-site to a friend

Copyright & disclaimer, Privacy policy